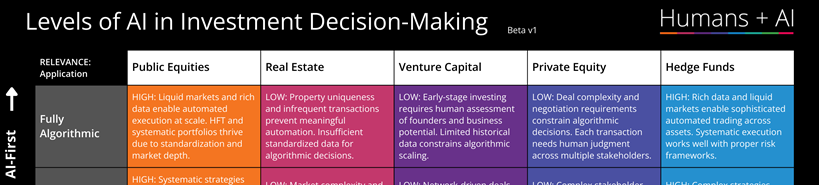

Framework: Levels of AI in Investment Decision-Making

AI has been used in investment decision-making for decades, with algorithmic trading a major market driver. Now the greatly broadened scope of generative AI is reshaping investment decision-making.

This framework is highly simplified, designed to draw out the spectrum from purely algorithmic decisions through to human-first decisions augmented by AI, across different asset classes. A few comments below.

Read more →