How will TV and digital video converge and who will take the bulk of the value?

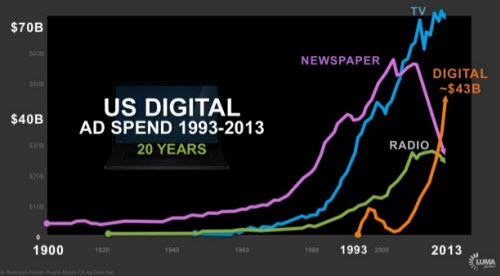

While news-on-paper is on the way out, it appears to be quite a different story for TV. The TV industry globally is challenged in a variety of ways, however revenues in the US remain resilient, as shown in this chart.

Source: LUMA’s The Future of (Digital) TV

Digital video has exploded over the last 8 years however that has, in the main, being a complement to TV, with TV viewing eroding surprisingly slowly compared to earlier forecasts.

While it seems a foregone conclusion that traditional TV and digital video will merge in a number of domains, including ownership, viewing, and potentially even distribution, how that happens is a more challenging question.

This very interesting presentation – below – from Terence Kawaja, CEO of media technology investment bank Luma, tells a nice structured story on how this convergence may happen.

Clearly the bank is talking up the convergence opportunities (which would often result in juicy investment banking fees), however the case they make is solid.

The presentation looks at the TV Business, Trends, Issues, and Theses. The trends it distills are pretty apparent, but well articulated:

1. Fragmentation

2. Device Proliferation

3. Second Screen

4. New Entrants

5. Original Content Production

In this industry both many of the incumbents as well as new entrants such as tech giants are well-capitalized. This means the structure of the convergence could be structured in a wide variety of ways, not necessarily led by the established firms.

No-one doubts that moving images will be a primary feature of our future, both in the formats we are used to today and far beyond.

The jury is still out on who will carve out the bulk of the value. One of the most encouraging things is that across almost all scenarios, there will be a very rich ecosystem for smaller producers and players to create value. There will be more creators, and an exceedingly large pie to share.