Seven Driving Forces Shaping Media

I earlier posted the Seven Driving Forces Shaping Media framework below, which was one of the frameworks included in our Future of Media Report 2008. However the framework is designed to cover an A3 sheet, so while it looks great in the printed copy of the report it can be hard to read on a screen. In addition many people don’t click through to pdfs. So I’ve posted this content in a blog-friendly and more readable format below.

Seven Driving Forces Shaping Media (pdf 700KB):

Since the event I’ve heard that the seven driving forces have been used in a range of presentations inside organizations and at conferences, and also in some executive strategy sessions. Before I created the visual summary of the trends I’d used them in a variety of client offsites and found they were useful in framing strategic thinking, all of which suggests it’s worth providing these again in a more accessible format.

If you like this framework, also see our Future of the Media Lifecyle Framework and Future of Media: Strategy Tools framework.

SEVEN DRIVING FORCES SHAPING MEDIA

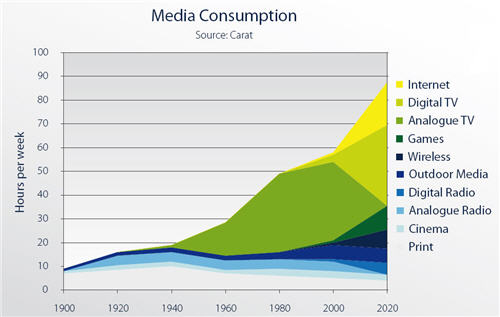

1. Increasing Media Consumption

Humans are intrinsically media animals. As we get greater access to media and content, we are discovering that our appetite for information and entertainment is virtually insatiable. It is commonplace for people of all ages to consume multiple media at the same time, with television, internet, newspaper, messaging, and other media frequently overlapping.

Implications:

Average total media consumption will exceed waking hours. Most media will be consumed with partial attention. Advertising impact will decrease.

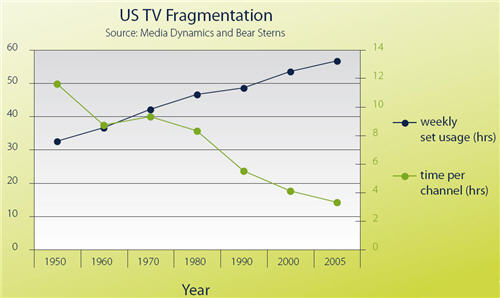

2. Fragmentation

At the same time as we are consuming more media, every existing media channel is being fragmented, and new ones are being added apace. In the example of television in this chart, we watch ever more television, but the proliferation of new channels means continually less viewer time per channel. Now that the Internet and mobile are creating an explosion of new channels and content, audiences are being divided into smaller and smaller segments.

Implications:

Current mass media markets are ephemeral. Revenues per channel will decrease. In all except a handful of cases, production costs will need to scaled down.

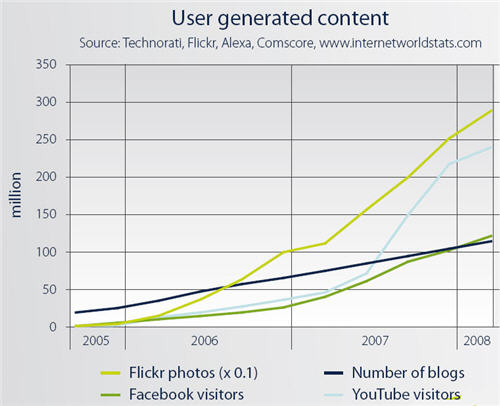

3. Participation

Early talk about consumer-generated media has become a stark reality over the last two years, with an explosion of media participation across blogs, photos, videos, social networks, and more. The costs of quality content creation are plummeting. Already a large proportion of content available is non-professional, and people’s media activities are increasingly focused on participatory channels such as social networks.

Implications:

An infinite supply of content. Increased fragmentation of attention. Pro-Am (professional-amateur) content models will emerge.

4. Personalization

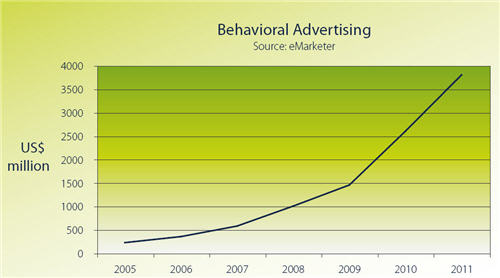

Media is becoming personalized. Ultimately this is about user control, in enabling every possible choice in what, when, and where people consume media, and its formatting, filtering, and presentation. At the same time, real-time information on viewers enables highly targeted advertising based on behaviors, location, and other profile data. The fate of personalized advertising will depend on how societal attitudes to privacy evolve.

Implications:

Users’ expectations for control over their media will increase. Abuse of personalized advertising will create a backlash. Some will opt-out, and others will opt-in if sufficient value is created.

5. New revenue models

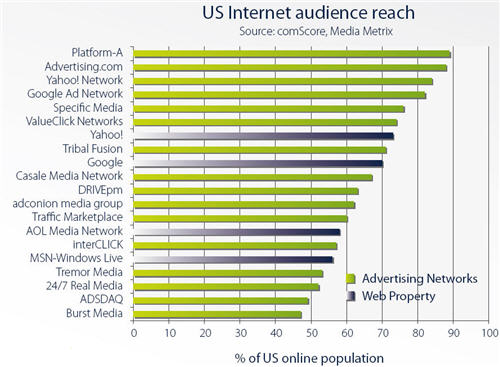

Within the current trend away from subscription and towards ad-supported business models, the way that advertising is sold is dramatically changing. As illustrated, the vast majority of the online players with the greatest reach are advertising networks, not stand-alone sites such as Google or Yahoo! Unbundling sales and content is allowing far greater scalability of content production costs. The promise of micropayments for content may re-emerge within a decade.

Implications:

Advertising aggregation will be central to the media landscape. Media companies will segment and unbundle ad sales and content creation.

6. Generational change

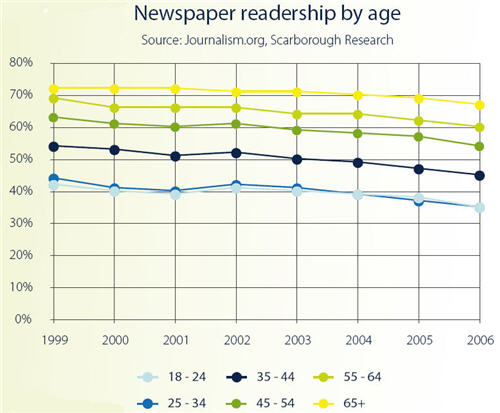

The chart shows that each generation is fairly consistent in its media consumption patterns, however that each group behaves very differently. The average audience age of traditional media such as television and radio continues to increase. Over the medium to long-term, generational change will result in dramatically different profiles for media consumption and participation.

Implications:

Media channels will be increasingly age-segmented. Advertisers will accelerate their shift to new media outlets. Sharemarket valuations will reflect age profiles of audiences.

7. Increasing bandwidth

In developed countries the Internet has now shifted from dial-up to broadband in the home. A rapid pace of increase in bandwidth will continue indefinitely. It will not be too long before the majority of developed country homes receive over 100Mbps. At the same time mobile bandwidth is soaring, with a variety of technologies contributing to pervasive high-speed access to content.

Implications:

Video on demand anywhere, anytime. Personal clouds will allow music and video collections to be accessed anywhere without local storage. The rationale for allocated media spectrum and infrastructure will fade.